Articles

Global Compliance Challenges & AI Verification in 220+ Countries

Learn how AI-powered verification helps businesses meet global KYC, AML, and fraud compliance requirements across 220+ countries and territories.

Articles

Learn how AI-powered verification helps businesses meet global KYC, AML, and fraud compliance requirements across 220+ countries and territories.

Articles

Businesses often accept screenshots, scans, and phone photos because they are easier to collect. But when native documents become pictures, important integrity signals can disappear. Here is why companies now need AI that can inspect both images and PDFs in the same fraud workflow.

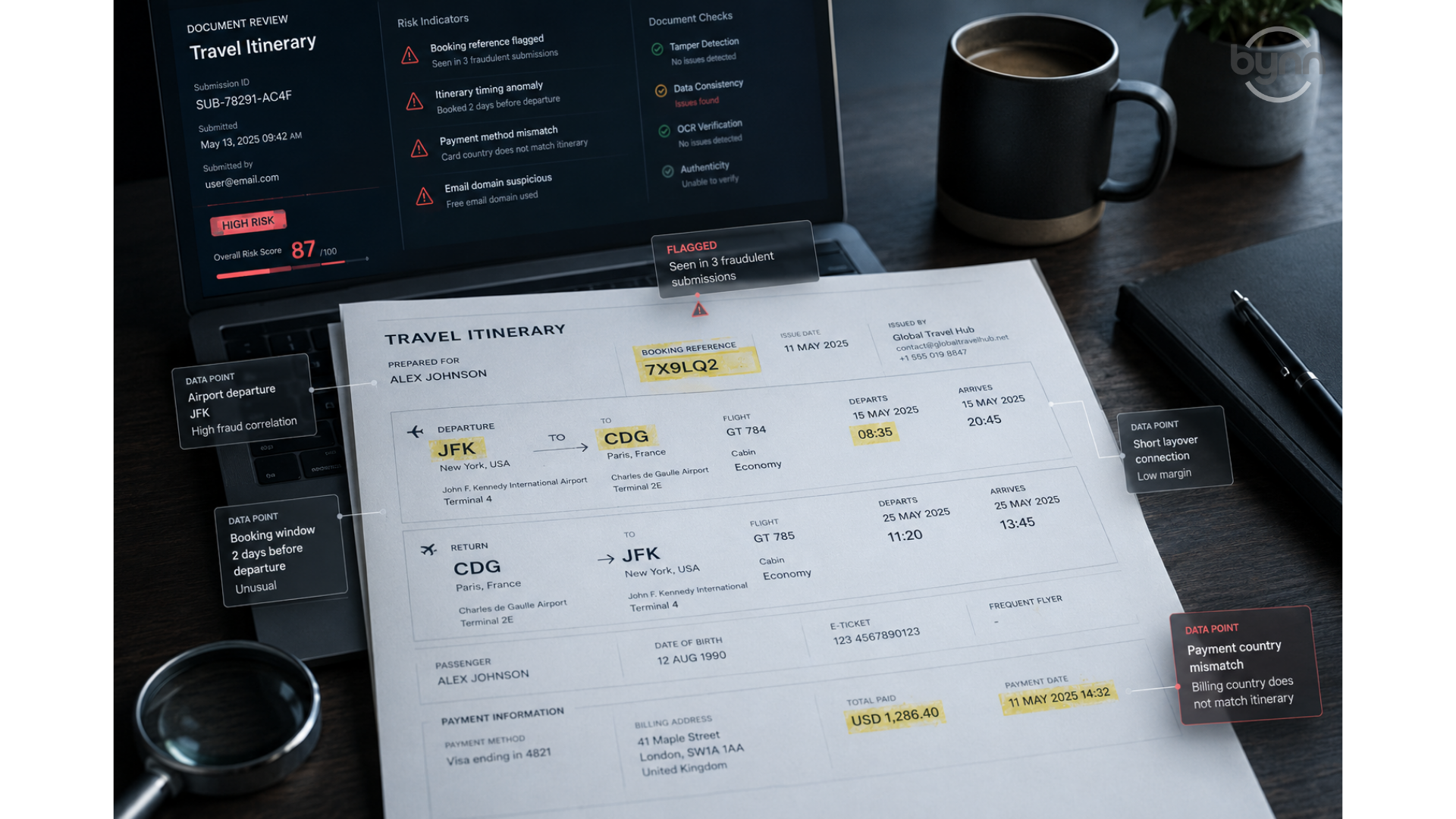

Articles

Fake travel itineraries can slip into visa files, claims, onboarding flows, and compliance reviews. Learn the red flags, verification steps, and how Bynn helps detect forged travel documents.

Articles

Discover how AI-powered fraud detection helps insurers identify fake claims, verify identities, and prevent losses. Learn how solutions like Bynn reduce risk, streamline claims, and improve compliance.

Articles

Learn how AI detects fake resumes, forged certificates, and identity fraud in hiring. Discover how Bynn helps organizations secure employee onboarding at scale.

Articles

Discover how AI detects forged IDs, passports, PDFs, and bank statements in under 10 seconds using forensic analysis, biometrics, and real-time KYC verification.

Articles

Discover the real cost of document fraud—from fake invoices to forged IDs—and learn how AI-powered verification from Bynn helps businesses prevent costly fraud.

No results

Try searching for another keyword.