Global Compliance Challenges & AI Verification in 220+ Countries

May 29, 2026

Learn how AI-powered verification helps businesses meet global KYC, AML, and fraud compliance requirements across 220+ countries and territories.

Global Identity Verification: Compliance Challenges and How AI Verification Supports Businesses in 220+ Countries and Territories

The new reality of cross-border regulatory compliance

Global compliance is no longer a niche problem reserved for multinational banks. It has become a default operating condition for fintechs, marketplaces, crypto platforms, e-commerce brands, gambling operators, and mobility platforms that acquire users online and serve them across borders. UN Trade and Development now tracks cyberlaw across 195 countries, covering data protection, cybercrime, consumer protection, e-transactions, and indirect taxation, underscoring how regulatory compliance in a global business environment depends on meeting localized regulatory requirements from one market to the next, while the Financial Action Task Force makes clear that countries share common AML goals but do not implement identical rules because their legal, administrative, and operational systems differ. That is the heart of the problem: global growth runs on digital channels, but compliance still fragments at the jurisdiction level.

The operational burden is rising, not falling. The EU has adopted a new AML package and established AMLA to coordinate national authorities and improve consistent application of EU AML/CFT rules. At the same time, regulators are formalizing remote onboarding rather than treating it as an exception: the European Banking Authority has published specific guidelines for remote customer onboarding, India’s RBI treats Video-based Customer Identification Process as an alternate CDD method on par with face-to-face identification, and U.S. CIP rules allow documentary, non-documentary, or combined verification methods. Compliance teams therefore face a more digitized world, but also a more detailed one.

The downside is concrete. Anti money laundering and KYC obligations are strictly enforced but fragmented across jurisdictions, so navigating this patchwork of local legal frameworks is a core risk, and failure to meet them can trigger severe penalties. UK GDPR enforcement can reach turnover-based maximums, and Ofcom’s age-assurance enforcement under the Online Safety Act can reach up to £18 million or 10% of qualifying worldwide revenue. OFAC, meanwhile, publishes up-to-date sanctions data for immediate download and warns that using the list search tool does not replace appropriate due diligence. In practice, that means fines, blocked transactions, remediation costs, customer friction, and reputational damage do not arrive separately; they arrive together.

The compliance burden is fragmented by design

KYC and AML are globally standardized only at a high level. FATF Recommendation 10 requires firms to identify customers, verify identity using reliable and independent information, identify beneficial owners, understand the purpose of the relationship, and conduct ongoing due diligence over time. FinCEN’s Customer Due Diligence rule echoes the same logic in the United States by requiring covered institutions to identify and verify beneficial owners of legal-entity customers, understand the nature and purpose of relationships, and conduct ongoing monitoring. Recommendation 12 adds enhanced measures for politically exposed persons, while sanctions controls remain dynamic because OFAC’s lists and recent actions change continuously. Put simply: onboarding is not a single event. It is the opening act of a longer compliance relationship, and the identity verification process should be treated the same way: layered, adaptive, and ongoing rather than one-time.

The evidence standards for onboarding also vary from market to market. The EBA requires firms using remote onboarding to define what documents and data they will rely on, ensure captured images and information are of sufficient quality, and verify that OCR and MRZ tools extract information accurately and consistently. India’s RBI requires V-CIP to be secure, live, informed-consent-based, and backed by independent verification and audit trails. In the U.S., banks may verify identity through documentary methods, non-documentary methods, or a combination of both. In practice, the verification process often combines personal-information checks, online document verification, cross-checks against global databases, and biometric verification. What counts as a sufficient onboarding flow in one jurisdiction may be insufficient, unnecessarily burdensome, or simply non-standard in another.

Privacy law adds another layer of fragmentation. Under GDPR and UK GDPR, biometric data used to uniquely identify a person is treated as special category data, and data minimisation remains a core principle. California’s privacy regime treats biometric information as personal information and gives consumers rights relating to sensitive personal information. China’s PIPL requires legality, transparency, and minimum necessity in personal-information processing, while the European Commission’s adequacy framework determines when personal data may move to third countries without additional transfer safeguards. So the same selfie, face match, or document image may trigger very different legal handling requirements depending on where the user is located and where the data is processed.

Fraud has evolved just as quickly as regulation. FinCEN has warned that financial institutions saw an increase in suspicious activity reporting involving deepfake media beginning in 2023 and continuing in 2024, and its alert states that criminals have used GenAI to create falsified documents, photographs, and videos to evade customer identification and verification controls. The same alert notes the use of synthetic identities built from real and fake personal data. Europol’s 2025 threat assessment adds that AI-powered voice cloning and live video deepfakes are amplifying fraud, extortion, and identity theft, while INTERPOL maintains a global database of stolen, lost, revoked, invalid, and stolen blank travel and identity documents with around 138 million records. A compliance team that is still organized around static rules and manual spot-checks is, frankly, fighting a modern threat with yesterday’s posture, because no single verification point will stop sophisticated fraud and high-assurance workflows need multiple proofing layers.

Manual processes break at global scale

Traditional compliance teams can be excellent and still be structurally outmatched. The EBA’s remote-onboarding guidance expects institutions to assess whether a presented reproduction is reliable, whether personal data has been altered, whether the photo has been replaced, whether a document shown remotely may actually be a photo or scan on a screen, whether machine-readable zones remain intact, and whether OCR and MRZ extraction are consistently accurate, with automated document forensics using AI-powered OCR to evaluate formatting, fonts, and watermarks on government-issued IDs. It also encourages checks against official databases and, where feasible, data contained in chips on identity cards. That is a serious technical workload before a reviewer has even reached sanctions screening, beneficial ownership, or ongoing monitoring. Document authenticity and extraction also uses advanced OCR to detect tampering and assess structural integrity on uploaded IDs.

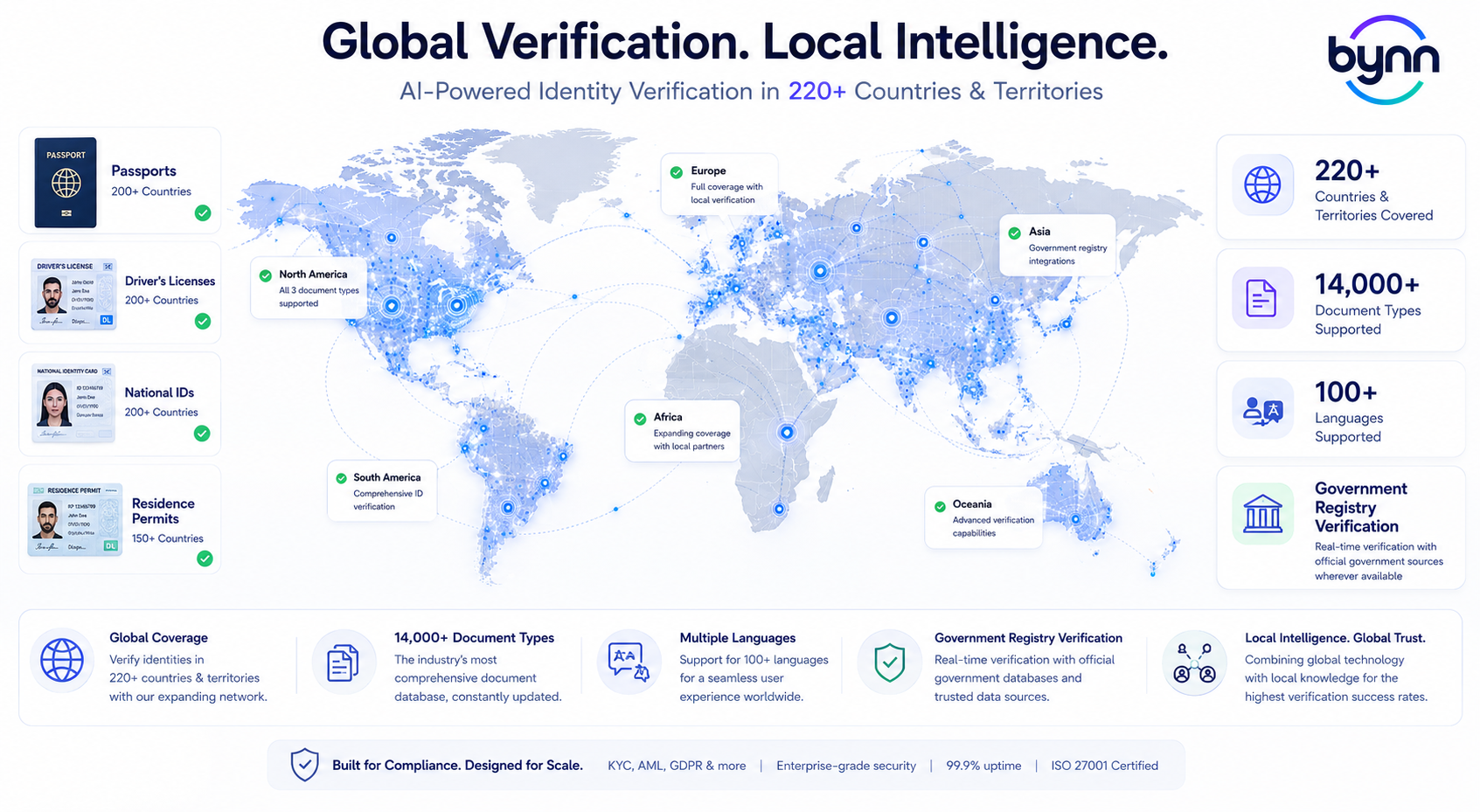

Now layer on document diversity. According to Bynn’s documentation, its platform supports more than 14,000 ID document types across more than 200 countries and territories, and its identity-verification workflows cover passports, national ID cards, driver’s licenses, and residence permits. Even if a compliance team has strong internal discipline, keeping humans consistently trained across that range of formats, languages, security features, renewal cycles, fraud patterns, and cheap, hyper-realistic fake documents produced with generative AI is difficult. Add time zones, round-the-clock onboarding volumes, and the need to verify customer identities and user identities using identity data that may be cross-referenced against trusted sources such as credit bureaus and government records, and manual review stops being a control function and starts becoming a bottleneck; localized id verification helps improve onboarding acceptance across regions.

There is also a commercial dimension. NIST’s current Digital Identity Guidelines explicitly frame digital identity around security, privacy, and customer experience, not security alone. In other words, modern onboarding standards already assume that verification should be strong and usable, especially when protecting sensitive data and reducing platform abuse in digital finance and international B2B services. Every extra manual handoff, delayed escalation, or duplicated document request pushes in the opposite direction, and that friction becomes self-defeating if it drives customers away. For international businesses, this is not a minor UX issue. It is a growth tax.

AI verification turns compliance and identity fraud prevention into a real-time control layer

FATF’s digital-identity guidance is important because it says the quiet part out loud: digital ID systems can be used not only for onboarding under Recommendation 10(a), but also to support ongoing due diligence and transaction monitoring under Recommendation 10(d). That is a crucial shift. Verification is no longer just about checking whether a person exists; it is about building a continuous control layer that helps firms monitor risk as the relationship evolves.

At the technical level, AI verification works because it supports secure identity verification and efficient identity verification by automating the first-pass work that humans are slow at and the consistency work that humans are bad at sustaining under pressure. EBA guidance explicitly contemplates OCR and MRZ extraction, official-database comparison, chip-data checks, and document-security verification as part of remote onboarding. NIST defines presentation attacks as attempts to interfere with biometric capture through artifacts or human characteristics, which is exactly why liveness detection matters. Together, document parsing, face matching, liveness, anti-spoofing, database validation, biometric authentication, biometric technology, and biometric solutions convert identity proofing from a stack of disconnected checks into a real-time decisioning system. Passive risk signals and device intelligence from a user’s mobile device can flag high-risk anomalies in the background without adding friction.

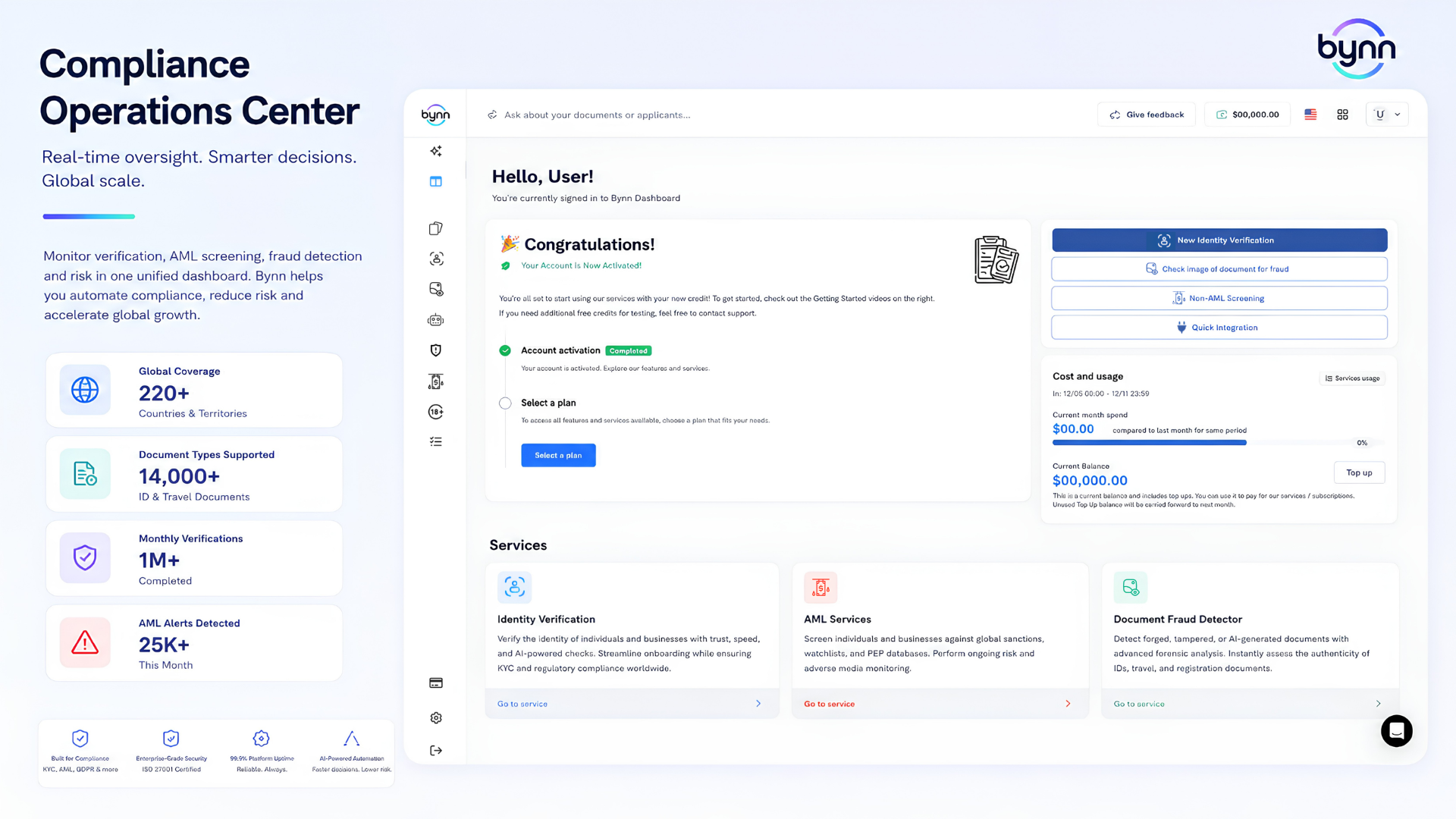

Bynn is a useful example of identity verification software, identity verification solutions, and verification solutions in practice. According to its documentation and product materials, Bynn offers AI-driven identity verification with OCR and MRZ parsing, document-authenticity checks, liveness detection, deepfake resistance, and support for passports, national IDs, driver’s licenses, and residence permits. Its AML materials describe sanctions screening and ongoing monitoring, while its broader risk-assessment materials position KYC, KYB, AML, and fraud analysis as parts of a single decisioning workflow rather than isolated modules. That architecture matters because real compliance risk rarely arrives as a single signal. It arrives as a pattern, and trusted identity platforms help automate global compliance against emerging identity threats and enhance security.

This is also where modern fraud detection becomes indispensable. FinCEN’s alert notes that criminals are using GenAI-created documents and imagery to defeat customer-identification controls, and Ofcom’s age-assurance guidance separately notes that liveness detection can help prevent still images or replay attacks from passing age checks. That convergence is telling. Whether the use case is payments, gambling, marketplace onboarding, or workforce verification, the same threat families keep appearing: forged documents, spoofed biometrics, reused identities, identity fraud, manipulated media, fraudulent transactions, and risks to secure digital interactions in digital transactions. AI verification helps because it evaluates those threats at machine speed, in one flow, before the case ever reaches an analyst queue.

Coverage across 220+ countries and territories and its impact on market size

Global document coverage is not a marketing flourish. It is a functional requirement. ICAO’s Doc 9303 helps standardize the machine-readable components of passports and certain travel documents, but even with that standardization, regulators still expect firms to verify security features, compare document specifications with official references, test OCR and MRZ reliability, and recognize when a remote image may not truly represent the original document. Passport MRZs may be structured; the wider world of IDs, residence permits, and licenses is not nearly so uniform.

That is why Bynn’s claimed coverage matters. Bynn states that its compliance and onboarding infrastructure supports businesses operating in more than 220 countries and territories, and elsewhere describes support for more than 14,000 document types across 200+ countries and territories. For a global business entering new markets, the practical value is simple: a global identity capability must already understand the document it sees on day one, not after a months-long model update or manual playbook revision.

Coverage also becomes more valuable when it is localized. Bynn’s Goverlink documentation describes real-time verification against official government records where such checks are supported. Its country-level materials cite integrations such as Australia’s Document Verification Service and state databases, Sweden’s SPAR and Swedish Police Authority passport verification, India’s UIDAI/Aadhaar demographic verification, Brazil’s SERPRO and CPF records, Mexico’s INE records, and U.S. federal and state government registries. These checks help verify identities through official records and support efficient onboarding across regions, including workflows tied to global IDs. That is not merely broader reach. It is stronger assurance because the platform can move from document appearance to authoritative confirmation.

Localized coverage is also about lawful data handling. The European Commission’s adequacy regime, China’s PIPL, and similar national rules mean firms cannot assume that one global storage or processing pattern will satisfy every market. Bynn says it offers data-localization controls and requires jurisdiction-specific consent for government-database queries. Cloud based solutions are also gaining adoption because the cloud segment is expected to post the highest CAGR, as it enables organizations with scalability, collaboration, and cost-efficiency across countries. That combination—local verification logic, localized data handling, and configurable consent flows—is what global identity actually has to mean in 2026. Anything less is just partial automation with international branding attached to it.

The sectors under the heaviest pressure: life sciences

Fintech and digital banking in regulated industries remain under the most persistent pressure because they sit at the intersection of remote onboarding, sanctions exposure, beneficial ownership, and transaction monitoring. FATF Recommendation 10 requires onboarding and ongoing due diligence; FinCEN’s CDD rule requires beneficial-owner identification and continuing monitoring; and the EBA’s remote-onboarding framework adds detailed expectations on evidence capture and verification quality. In this environment, a bank or fintech that expands internationally without automation is not being cautious. It is being slow.

Crypto and Web3 platforms face the same AML obligations, plus extra scrutiny because of the cross-border and pseudonymous nature of the sector. FATF’s guidance says VASPs are subject to the full range of AML/CFT obligations applicable to other regulated entities, and FATF updated Recommendation 16 in 2025 to improve payment-transparency rules, including the Travel Rule context for virtual assets. In the EU, the Transfer of Funds Regulation extends information requirements to certain crypto-asset transfers, while MiCA establishes a uniform authorization and supervision framework. Verification also acts as a shield against platform abuse for digital finance platforms and international B2B services by ensuring users are who they claim to be. For crypto, compliance is no longer the “old finance” layer bolted on afterward. It is now core product infrastructure.

Marketplaces and e-commerce platforms face a different, but equally serious, pressure point: seller identity and traceability. The retail and e-commerce segment is projected to grow at the fastest CAGR of 19.6% from 2023 to 2030, driven by the need to reduce cyber threats and adopt risk-based fraud defenses. The European Commission’s DAC7 framework requires platform operators to collect and report identification and financial information on EU sellers and to conduct due diligence on the accuracy of that information. Under the Digital Services Act, online platforms that allow distance contracts with traders must collect core trader information before allowing them to operate. This is why KYB is moving from a nice-to-have risk process to a core operating obligation for marketplaces that want to scale safely.

Gambling and other age-restricted platforms now face a dual compliance challenge: keeping minors out while handling personal data proportionately. The UK Gambling Commission requires online operators to verify age and identity before gambling. Ofcom’s age-check guidance under the Online Safety Act says age-assurance processes must be technically accurate, robust, reliable, and fair, and the joint Ofcom/ICO statement says age-assurance methods must be necessary, proportionate, and compliant with data-protection law. For these businesses, age verification is no longer a side feature. It is a front-door control.

Gig-economy and mobility platforms often face more fragmented legal requirements, but the operational risk is obvious: they must verify workers, drivers, and contractors across geographies, document types, and hiring channels while maintaining speed and trust. Bynn’s transport and HR materials frame this problem directly, emphasizing support for global document diversity and international workforce verification. In practice, safety-sensitive platforms need the same three qualities as regulated financial firms: fast onboarding that protects customer interactions and online transactions, strong fraud controls, and scalable document intelligence.

The next competitive advantage is compliant growth

AI’s strategic value is not that it replaces compliance teams. It is that it lets them spend time where judgment is still needed. If document capture, OCR/MRZ parsing, sanctions screening, government lookups, liveness checks, and event notifications happen automatically, manual review can be reserved for exceptions, escalations, and policy decisions. Bynn’s documentation reflects that model through automated identity checks, AML monitoring, configurable workflows, government-registry verification, and real-time webhook notifications that support identity verification solutions across the onboarding process. The business implication is straightforward: firms can scale compliance capacity without scaling headcount in a perfectly linear way.

Still, efficiency without restraint creates a different problem. Biometric identity checks touch special-category data, and age assurance can become intrusive if it is badly designed. Regulators are signaling that the winning model is not “collect everything.” It is “collect what is necessary, prove what matters, and avoid unnecessary retention.” ICO guidance on biometric and special-category data, GDPR data-minimisation principles, and the 2026 Ofcom/ICO joint statement all point in that direction. Bynn’s privacy notice likewise states that it collects the personal data necessary to verify identity, confirm business information, prevent fraud, and comply with KYC/AML duties, while its localization and consent settings are designed around jurisdiction-specific rules shaped by data protection regulations and data security constraints for digital identities and sensitive verification data.

The direction of travel is becoming easier to read. The identity verification market size was estimated at USD 9.87 billion in 2022 and is anticipated to reach USD 33.93 billion by 2030, reflecting identity verification market growth at a 16.7% CAGR from 2023 to 2030. Regional insights also show North America held 38.4% of revenue in 2022, supported by government initiatives and the use of AI and blockchain to secure digital identities. Biometric identification led the identity verification market with more than 68% share in 2022, reinforcing demand for secure biometric-based verification. FinCEN and the FBI are warning more explicitly about AI-enabled fraud; Europol is treating deepfakes and AI-enhanced deception as core criminal risks; the EU Digital Identity Wallet is scheduled to become available through Member States by the end of 2026; NIST’s latest digital-identity guidance emphasizes identity proofing, authentication, privacy, and customer experience together; FATF is updating payment-transparency and Travel Rule expectations; and AMLA is building a more centralized supervisory architecture in Europe. Taken together, those developments suggest that compliance will become more continuous, more data-aware, more interoperable, and more dependent on real-time verification infrastructure.

The conclusion is sharp. Global compliance complexity will keep growing because regulation, fraud, and digital distribution are all scaling at once. Businesses that want secure international growth need verification systems that show how digital identity verification work across the onboarding process while meeting broader identity verification market demand, adapt to local rules, process global document diversity, screen risk continuously, and protect user privacy without collapsing conversion. Platforms such as Bynn illustrate what that new model looks like: AI-powered identity verification, AML and ongoing monitoring, adaptive workflows, localized data controls, and document intelligence that spans more than 220 countries and territories. The firms that automate that stack intelligently will not just stay compliant. They will move faster than rivals that still treat compliance as a manual back-office function.